With an economic recession looming as part of Australia's post-lockdown recovery, some small business owners are lying awake at night wondering how to create a recession-proof business. Here are four tangible things you can do now.

In this article, I’ll try to answer these questions:

- Are we in a recession in 2022?

- How can I minimise the impact of an economic recession?

- What causes an economic recession?

- What is the difference between a recession and a depression?

- How could a recession impact my business?

Are we in a recession in 2022?

Interest rate rises have put the brakes on the Australian economy in an effort to curb rising inflation, after the world's economy recovered more quickly than expected from the pandemic.

At least two more interest rate rises are likely, according to the Reserve Bank of Australia (RBA), which could increase the likelihood of a recession in this country.

The situation in Australia is "on a knife's edge," according to the RBA deputy governor.

The Bank of England says Britain is probably already in recession, there are growing concerns about the United States, and China's economy is also straining under the pressure.

ANZ CEO Shayne Elliott says that 70% of the bank’s mortgage borrowers are ahead on their repayments. This could soften the blow of rising interest rates here at home.

In short, Australia may be heading into a recession because of:

- Rising interest rates

- High inflation

- Slowing economic activity after a post-pandemic high

Current events such as supply chain disruptions and the war in Ukraine are also impacting the global economy. Talk of a recession can also be a self-fulfilling prophecy, as it impacts on consumer confidence and spending.

RBA officials say that, at this point, they still have confidence Australia can avoid a recession during the next few business cycles. But time will tell.

How can I minimise the impact of an economic recession?

In a recession, people curb their non-essential "discretionary" spending. Those businesses that sell the essentials (e.g. groceries, medicine) naturally tend to fare better than those selling luxuries that people can live without.

But even if your business relies on a slice of people's discretionary "wants" budget, there are still plenty of things you can do to reduce the impact of an economic recession on your business.

A few hours of planning will pay off in less stress for you throughout an economic downturn, should it come.

1. Get your finances in order

If you've always been a bit lax when it comes to the financial side of your business, then now is the time to get into good habits.

Firstly, go through your accounts and collect any balances due to you.

If you still rely on shoebox accounting, or you manage your finances using a jumble of complicated spreadsheets, now might be the time to finally upgrade to using proper accounting software. Check out our top picks, including two free apps, here.

Along with saving you a lot of time and effort, accounting software also makes it much easier to get an accurate picture of your business' financial health and stay on top of outstanding debts.

If you can, be flexible about payment, as everyone is in the same predicament. For example, allowing clients to pay in installments is better than not getting paid at all.

Remember, when economic growth kicks in again, this kind of goodwill can help forge long-term business relationships.

Review the terms of your debts

Once that’s done, take a look at your loans and debts to see where you can save, consolidate or restructure. Once again, upgrading to proper accounting and finance software can help here.

- Consider the merits of a business loan or line of credit.

- Talk to your accountant about your eligibility for business hardship grants.

- If things are really tight this business cycle, you might ask about deferring payments on your home or business loans. But keep in mind there's a long-term cost because the interest keeps stacking up.

Resist the temptation to draw on your superannuation, as even a small withdrawal now can have a significant long-term impact on your retirement savings.

Consider a home loan offset account

Money might be tight, but economic recessions are actually a good time to put extra cash into your home loan, so you're paying off more of the principal. If you pay tax and GST quarterly, consider keeping that money in a home loan offset account so it's reducing the interest you pay on your home loan.

When tax money is sitting in your offset account before you hand it over to the ATO, that money is working much harder for you than if it was sitting in a savings account, where it would be making minimal interest on which you'd pay tax.

2. Redo your budget

The next step in preparing for N economic recession is to look at both your personal and business budgets, which might be intertwined if you're a small business owner.

If you've never drawn up a proper list of your income and expenses, do it now.

When it comes to your personal finances, a 50/30/20 budget is a good starting point. So:

- 50% of your income goes towards necessities

- 30% towards wants

- 20% towards saving, investing and repaying debt

When drawing up your personal and business budgets, look for areas where you can trim expenses such as cutting back on luxuries and putting some services on hold or dropping down a tier for the next few business cycles.

Consider where it might be more efficient to outsource some business functions, as well as which tasks you might bring back in-house if you'll have more time on your hands during the recession.

It's not just about cutting costs and boosting income to ensure that you bring in more than you spend. It's also about building up an emergency cash reserve as a buffer, planning for the future and investing in ways that grow your business.

Related: Could your small business save with a VOIP phone system?

3. Review your products and services

Remember, all your customers are also considering how they can tighten their belts, so you need to think about what you can do to ensure your products or services are as appealing as possible.

Streamline your inventory

Inventory management can be tricky at the best of times, but it's especially important during a recession. Holding too much inventory can reduce your cash reserves without adding to sales, while too little inventory can result in lost sales.

Consider discounting

This is where you need to look over your historical data, industry insight and economic forecasts to develop your sales forecasts and optimise your pricing strategy, perhaps including strategic discounting.

Actively look for new opportunities

Don't simply weather out the storm to discover your competitors have emerged strong — look for strategic opportunities to expand into new areas, develop new products and target new customers in different regions.

If your business depends on a slice of your customers' "wants" budget, then undertake some market research to determine what you can do to dip into their "needs" budgets.

Look at your products and services with a critical eye

The same goes for the mix of services you provide.

Are there less profitable products or services that might be worth adapting or dropping?

If you’ve been charging on a yearly basis for your service, consider switching to a budget-friendly monthly or quarterly billing option.

Remember to be considerate of your customers' needs and aim to be flexible where possible, especially if you're in the services industry. You'll rely on these customers when the economy picks up again, so try to keep them onside. You need to play the long game.

Related: 8 customer retention tips when you have to raise prices

4. Use your downtime wisely

If business is slow due to the economic recession, don't just flop down on the couch. Use some of that time to work "on" the business rather than "in" the business.

Think about those tasks you've been putting off, such as:

- Taking stock of your business

- Upgrading systems

- Updating processes

- Overhauling your website

Talk to other business owners in your industry to gather insight and share ideas on creative ways to weather the downturn.

Editor’s note: Working for yourself? GoDaddy can help set you up with its free logo maker, free website builder and productivity tools like Microsoft 365, including the world-famous suite of products (Excel, PowerPoint, etc).

What causes an economic recession?

An economic recession is basically when the economy starts shrinking rather than growing. Economists typically define it as two or more consecutive quarters of negative gross domestic product (GDP) growth, which is the total value of everything that a country produces.

The end of a recession is marked by the point where the economy returns to GDP growth, not the point where it eventually returns to an economy's original pre-recession position.

The last major Australian recession was between 1990 and 1992, when the unemployment rate hit a high of 12%. There was also a short-lived recession in 2020 as the pandemic and lockdowns took their toll on the economy.

Recessions can be caused by a range of factors, including:

- Economic shocks

Unpredictable events can cause widespread economic disruption, from wars and terrorist attacks to natural disasters and pandemics such as the COVID-19 outbreak.

- Loss of consumer confidence

When people are worried about the economy, and perhaps concerned about job security, they tend to reduce their spending and save money where they can. Considering that almost 70% of GDP depends on consumer spending, a loss of consumer confidence can see the entire economy slow drastically.

- High interest rates

Interest rate rises are designed to slow down an overheated economy which is expanding at an unsustainable rate and is in danger of faltering. This is a delicate balancing act. High interest rates make it expensive for people to borrow money, which means they spend less. Businesses also reduce their spending and growth plans because the cost of financing is too high. Yet if interest rates go too high, they can trigger a recession.

- Deflation

The opposite of inflation, deflation is when product and asset prices fall because of a large drop in demand. Consumers can see this downward trend and wait for prices to fall even further, creating a downward spiral which reduces economic activity.

- Asset bubbles

Whether it's tech stocks in the dot-com era or the real estate boom, sometimes the price of certain investments can rise rapidly, far beyond their true worth. This artificial demand inflates the bubble, but eventually it bursts. At this point, people lose money and consumer confidence plunges. People and businesses then cut down on spending and the economy can go into recession.

What is the difference between a recession and a depression?

Recessions are considered a normal part of the economic cycle, due to peaks and troughs in GDP.

A recession occurs when GDP shrinks for at least two quarters; a depression is an extreme fall in economic activity that lasts for years.

The Great Depression occurred after the stock market crash of 1929 and its effects were felt around the world for a decade. Worldwide GDP plunged by an estimated 15%.

New laws and regulations were introduced to prevent a repeat of the Great Depression. Central banks and policymakers around the world have changed the way they tackle economic stagnation, to reduce the likelihood of a recession turning into another depression.

Today, central banks like Australia's RBA are quick to use policies to lift the economy during a downturn.

This helped ensure that the global recession of 2009, triggered by the Global Financial Crisis (GFC), did not turn into another full-blown depression.

Australia was one of the few countries to avoid a recession after the GFC in 2009, in part due to monetary policy and continuing strong demand from China for its natural resources.

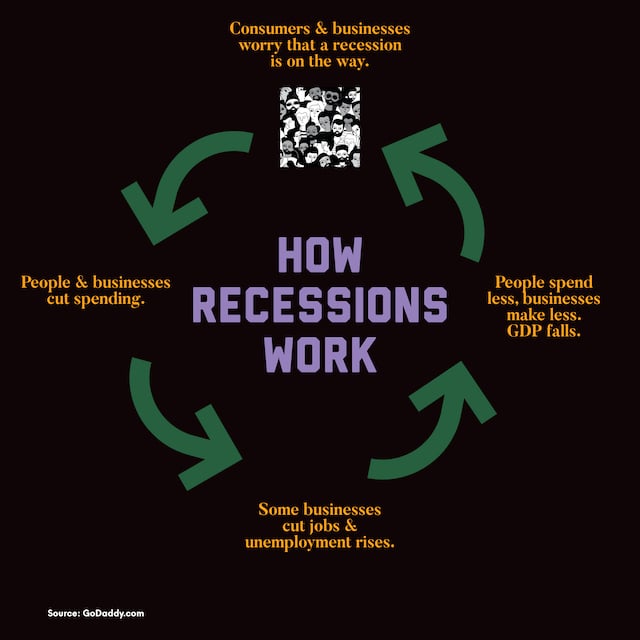

How could a recession impact my business?

As mentioned, recessions occur when there's a significant decline in economic activity, such as businesses and consumers cutting back on spending. This hurts business, which leads to a depressed labor market, which further reduces consumer confidence and spending as people have less money to spend.

Even those who are still working may worry about job security.

Apart from a decline in real GDP, other impacts of a recession can include a:

- Decline in real income

- High unemployment rate

- Stagnation of manufacturing

- Decline in retail sales

- Drop in consumer spending

Most recessions only last for around 12 months, although some may take years to turn around due to the flow-on effects.

The impact on your business could include reduced sales and profits, impeded cash flow and limited lines of credit.

These can see businesses stuck in a vicious cycle. As consumer and business spending drops, businesses see sales drop, which forces them to cut their own spending and overheads. This in turn sees incomes fall and jobs lost elsewhere, which leads to a further drop in consumer and business spending.

When money is tight, customers can also be slower to pay, putting a significant strain on your cash flow. Some of your customers can also go out of business during a recession, leaving unpaid debts. This in turn makes it more difficult for your business to pay its own suppliers, creating a flow-on effect.

At the same time, lenders such as banks can tighten their belts, making it more difficult for your businesses to access the usual lines of credit. As interest rates increase, lending requirements become stricter to ensure that businesses can afford to repay their loans.

In the long-term, economic recessions tend to bring lower interest rates and government-led economic stimulus packages in an attempt to kick-start the economy. These can ease the impact of the recession on your business and help you bounce back strong.

The information contained in this blog post is provided for informational purposes only, and should not be construed as an endorsement or advice from GoDaddy on any subject matter. Seek financial advice from a professional before making any changes to your small business.

UPDATE: This article on economic recession was first published on 5 November 2020 and updated October 2022 and again 28 October 2022.