As a small business owner, it's essential to keep on top of your numbers. This means making sure the books are balanced, but sometimes there may be some anomalies leaving you scratching your head. To help with finding the root cause, you use a trial balance.

When we're going on about our business, it's easy to lose sight of our incomings and outgoings.

The purpose of the trial balance is to correct mistakes that could hurt your business.

The best bit is that it's simple to produce and you don't need an accounting degree!

What is the purpose of a trial balance?

A trial balance is a simple accounting report you produce that lists each account name and the balance documented within the general ledger. Note that this check is not necessary for those using reputable accounting software to manage their business finances.

The account balances are in two columns: debits and credits. At a glance, the report clearly shows you whether your debits and credits are equal to one another.

If your debits and credits do not match, there’s something amiss in the numbers. The inaccuracy could be from incorrectly entering debits and/or credits. But don't worry — the purpose of a trial balance is to proactively find and fix errors as these can be quite common.

Trial balance reports should be prepared at the end of each reporting period. Not only does it give you confidence that your books are on point, it will save you from the auditors and possible penalties.

How to prepare a trial balance

When preparing a trial balance, you will need your general ledger information.

The general ledger provides a record of each financial transaction that occurs during the lifespan of your business.

You then add all the accounts and dollar amounts from your books to your trial balance worksheet. Separate them into debits and credits by account type. You should have three columns:

Accounts

An account is a record in the general ledger that is used to sort and store similar transactions.

For example, businesses will have a:

- Cash account, recording every transaction that increases or decreases the business’s cash

- Sales account that shows all the amounts from the sale of products and/or services

Debits

A debit is an accounting entry that can either increase an asset or expense account (or decrease a liability or equity account). This is positioned in the left column of a trial balance.

Credits

A credit is an accounting entry that either increase a liability or equity account (or decreases an asset or expense account). This is positioned in the right column.

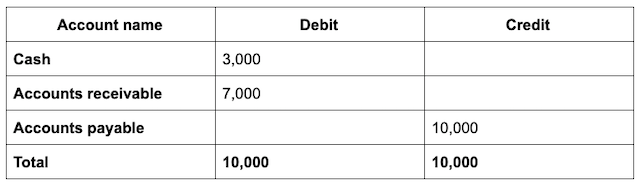

Once you have entered all the information into your trial balance worksheet, you need to add up each column. The total of the debit column and credit column should be equal, which then means you have a balanced trial balance.

You have an unbalanced trial balance when the two numbers are unequal. You will then need to find out why the totals don't add up and adjust accordingly.

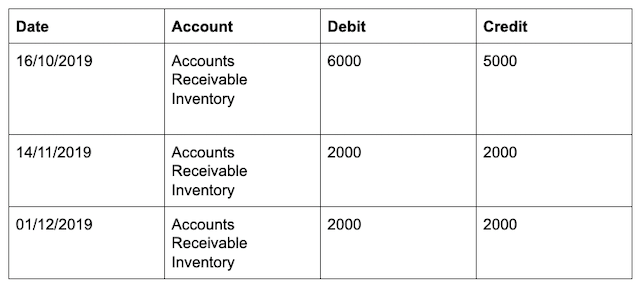

An example of an unbalanced trial balance

Sometimes, your debits and credits are unequal. If an entry has been mistakenly entered, it will create an unbalanced trial balance.

When you see the discrepancy, you will need to go back to your general ledger to find where the error is.

You can start by looking into your accounts receivable (money owed to you but not yet received) and inventory entries.

We can we see in the trial balance example above that the first entry created on 16/10 is unbalanced. There is a debit of $6,000, but only $5,000 was credited for inventory. This leaves a $1,000 discrepancy. Now that we know where the error is, you can go back and adjust the trial balance. Error found and corrected!

What happens after the trial balance?

A balanced trial balance is not only music to your accountant's ears, but it is a reflection of your business’s health. What’s more, it’s the foundation for the three basic financial statements all businesses need:

- Income statement

- Balance sheet

- Cash flow statement

You can use all these financial statements to make smarter decisions about your business — like whether to cut expenses or look into the reason behind why sales are not picking up in a certain period.

Many accounting apps do not allow users to enter unbalanced entries into the general ledger.

This means the trial balance is not needed by businesses that are using the software.

If you're still using manual record-keeping for your business, then the trial balance has more value, as there is more room for human error when it's manual.

Time to go digital?

Once your business is up and running and cash flow is moving, it may be a good opportunity to consider investing in a good accounting software such as QuickBooks, Xero or Sage. At a bare minimum, an Excel spreadsheet should suffice.

Otherwise, if you have a million other things you would rather do, hire a bookkeeper to help you stay on top of your income, expenses and recording-keeping of receipts and invoices.

Sometimes outsourcing this can be more cost-effective because you only need to pay for a couple of hours work a month (usually two to four hours) rather than a wage. And because they are experts, you are getting professional and accurate work done that should satisfy the Australian Taxation Office.