As a business owner, have you ever wondered how those online payments actually go through? It might seem like magic, but there's a key piece of technology working behind the scenes: the payment gateway.

Think of it as the secure bridge that connects your customer's payment to your business bank account. Let's take a closer look at what a payment gateway is and how it helps you get paid.

Level up your payment processing with GoDaddy Payments.

What is a payment gateway?

A payment gateway is the technology that acts like a virtual point-of-sale terminal for online and in-person transactions. In technical terms, it's an infrastructure that securely transmits payment information between a customer, a merchant, and a payment processor.

Think of it as a secure tunnel that encrypts sensitive data, like credit card details, during a purchase.

For those less familiar with the tech side, imagine a payment gateway as the helpful assistant at an online store's checkout. When you enter your payment information, this assistant verifies your details and communicates with your bank and the store's bank to ensure the transaction is legitimate and goes through without a hitch. It's the behind-the-scenes magic that allows you to buy things online with confidence.

How does a payment gateway work?

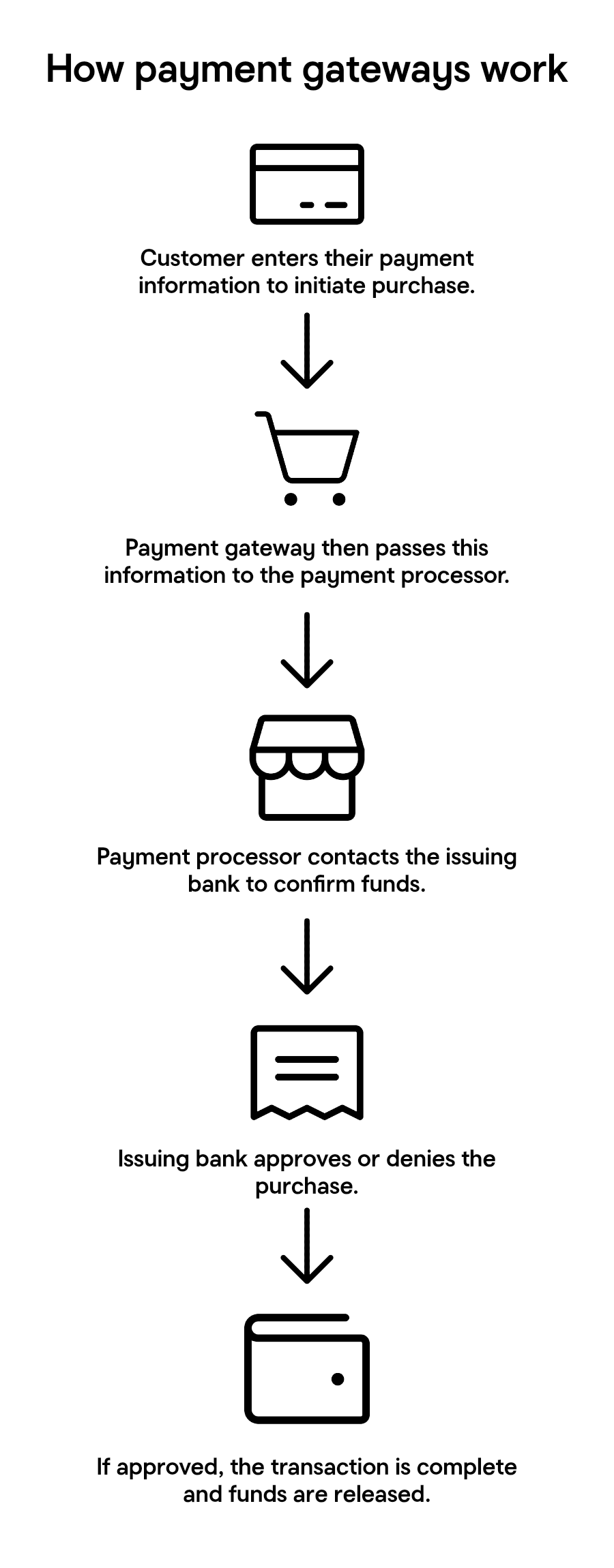

Think of a payment gateway as the behind-the-scenes process that makes online purchases possible. Here's a simplified view:

- Customer initiates a purchase: The customer selects items and proceeds to checkout on a website or app.

- Payment information is entered: The customer enters their credit card or other payment details. This sensitive data is encrypted by the website.

- Transaction request is sent: The encrypted data is sent to the payment gateway.

- Gateway routes the transaction: The payment gateway acts as a secure intermediary, routing the transaction information to the payment processor.

- Payment processor contacts the card network: The payment processor sends the transaction details to the appropriate card network (like Visa, Mastercard, etc.).

- Authorization request: The card network sends an authorization request to the customer's bank.

- Bank approves or declines: The customer's bank approves or declines the transaction based on available funds and other factors.

- Response is relayed: The bank's response is sent back through the card network, to the payment processor, then to the payment gateway.

- Merchant receives the response: The payment gateway communicates the transaction status (approved or declined) to the merchant.

- Transaction is completed: If approved, the merchant fulfills the order.

Example of a payment gateway

Consider GoDaddy Payments. When a customer buys online, it securely captures and encrypts payment details, sending them to the processor for bank verification. Approval or denial is relayed back, informing the merchant and customer.

GoDaddy Payments also streamlines in-person sales with tap-to-pay and offers a mobile app for managing transactions, receipts, payouts, and refunds within the GoDaddy ecosystem, simplifying payment processing for your business.

What does a payment gateway do?

A payment gateway offers several key features and functionalities to streamline payment processing for your business:

- Securely transmits payment data: It encrypts sensitive customer information during transactions, protecting it from potential breaches.

- Authorizes transactions: It communicates with payment processors and card networks to verify funds and ensure the transaction is legitimate.

- Facilitates different payment methods: Gateways often support various payment options, including credit and debit cards, and sometimes digital wallets or other local payment methods.

- Provides transaction reporting: Many gateways offer dashboards and reports to help you track sales and manage your payment history.

- Integrates with ecommerce platforms: They typically connect seamlessly with an ecommerce website and a point-of-sale system.

- Helps with fraud prevention: Gateways often have built-in tools or integrations to help identify and prevent fraudulent transactions.

What to look for in a payment gateway

Choosing the right payment gateway is crucial. Here are key features, both product and company-related, to consider:

- Security: Look for PCI DSS compliance and strong encryption.

- Accepted Payment Methods: Ensure it supports the cards and digital wallets your customers prefer.

- Fees and Pricing: Understand processing fees, monthly costs, and other charges

- Ease of Integration: Check compatibility with your website or POS system.

- Customer Support: Opt for reliable and responsive assistance.

- User-Friendliness: The system should be easy for you and your customers.

- Reporting and Analytics: Access to clear sales data is important.

- Scalability: Choose a gateway that can grow with your business.

- Additional Features: Consider options like recurring billing and fraud prevention.

Payment gateway vs payment processor

While often discussed together, a payment gateway and a payment processor serve distinct roles in the transaction process:

- Payment gateway: Think of the gateway as the secure connection between the customer, the merchant, and the payment processor. It securely transmits the customer's payment information to the processor and relays the transaction response (approval or decline) back to the merchant. It's like the messenger ensuring secure communication.

- Payment processor: The payment processor is the infrastructure that actually handles the transaction. It communicates with the card networks (like Visa, Mastercard, Apple Pay, Google Pay, etc.) and the banks involved to move the funds from the customer's account to the merchant's account. They are the ones doing the heavy lifting of the financial transaction.

The payment gateway is primarily focused on secure communication and routing of transaction data. The payment processor is focused on the actual clearing and settlement of funds. Most businesses need both a payment gateway and a payment processor to accept electronic payments seamlessly. Often, these services are bundled together by a single provider for simplicity.

Payment gateway vs. bank

While both are essential for handling finances, payment gateways and banks serve different functions in the context of business transactions:

- Bank: Your business bank account is where your funds are ultimately held. It's a financial institution that provides services like checking and savings accounts, loans, and other financial management tools. When a customer pays you, the money eventually lands in your business bank account. Your bank is the central hub for your business's finances.

- Payment gateway: As we've discussed, a payment gateway is the technology that facilitates the secure transfer of payment information during a transaction. It acts as an intermediary, ensuring the data from your customer's payment method reaches the payment processor and the transaction result returns to you. The gateway doesn't hold funds; it simply moves the necessary information.

Think of your bank as the destination for your earnings, while the payment gateway is the secure road that the payment travels on to get there. You need a bank account to receive funds, and if you're accepting electronic payments, you typically need a payment gateway to process those transactions securely and efficiently. They work in tandem to ensure you get paid.

Payment gateway vs. payment terminal

Understanding the difference between a payment gateway, which handles online transactions, and a payment terminal, used for in-person sales, is key for any business that interacts with customers in more than one way.

- Payment gateway: This is the digital infrastructure that facilitates online payment processing. It securely transmits payment information from the customer's browser or device to the payment processor and then communicates the transaction result back to the website or application. Think of it as the virtual connection that enables ecommerce transactions.

- Payment terminal: This is hardware used at a physical point of sale used to process in-person payments. These can range from basic card readers to more comprehensive POS systems. They interact directly with physical credit or debit cards or mobile payment methods like tap-to-pay, often explained in resources like what is a POS.

The fundamental difference lies in their environment. Payment gateways are essential for online businesses to accept digital payments securely. Payment terminals are necessary for brick-and-mortar stores to process transactions made with physical cards or devices. While both aim to facilitate payments, they operate in distinct channels to serve different customer interaction models.

Types of payment gateways

Depending on your technical capabilities and business needs, you can choose from three main types of payment gateways:

- Hosted gateways: The most user-friendly option for businesses with limited technical resources. Implementation involves simply embedding a link or button on your website that redirects customers to the payment service provider's platform to complete their purchase. This requires minimal technical setup, but gives you less control over the checkout experience.

- Self-hosted gateways: With this option, your business manages the payment interface and data capture directly on your website. While this provides greater control over the customer experience, it requires significant technical expertise for initial setup and integration. You'll also take on more responsibility for security compliance.

- API-hosted gateways: These gateways require technical knowledge to implement, particularly for making API calls and handling responses within your own application. However, they offer a balance between control and convenience, allowing you to customize the payment experience while leveraging the provider's secure infrastructure.

- PayFac as a Service: Providers utilize API-hosted gateways to facilitate the secure and seamless processing of online payments for their sub-merchants.

Do I really need a payment gateway?

If you're running an ecommerce business and want to accept online payments, the answer is yes—you need a payment gateway. A payment gateway serves as the crucial intermediary that securely processes transactions between your customers and your business bank account. Without one, you cannot accept online payments.