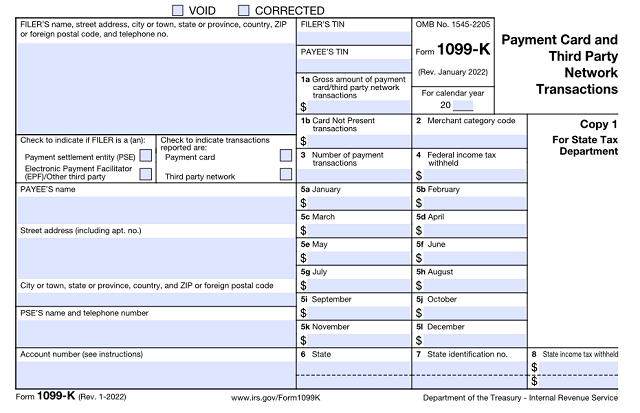

It’s tax season and that means that all manner of mysterious tax forms might begin appearing in our mailboxes. The tax forms that small business owners end up with can be even more perplexing — especially if you’re new to entrepreneurship. What the heck is this 1099-K form? Why did you receive it? What does it all mean?

Your business needs a website.

We’ll cover all of these questions below.

Disclaimer: This content should not be construed as legal or financial advice. Always consult an attorney or financial advisor regarding your specific legal or financial situation.

What is Form 1099-K?

Form 1099-K debuted back in 2012 when the government was attempting to find more funds (aka collect more taxes) after the 2008 financial crisis.

Third-party payment processors such as PayPal, Amazon, and Stripe are required to issue Form 1099-K to certain merchants who use those processors to process payments.

The government’s thinking went that perhaps merchants who used these third-party payment processors to collect money weren’t paying taxes on that income. These days, those third-party payment processors are required to send form 1099-K to both businesses using their platforms and the IRS.

In other words, form 1099-K is the government’s way of tracking how much money really passes through online payment processors such as PayPal, Amazon, and Stripe.

Related: Are you making business taxes more complicated than they need to be?

Who receives Form 1099-K?

Form 1099-K has been around since January 2012, but you might not have received it. That’s because you have to meet some specific criteria in order to get the form. Third-party payment processors are required to send form 1099-K to people who:

- Made more than $20,000 in sales volume through that specific payment processor.

- Made over 200 sales through that specific payment processor.

Note: In 2021, it was decided that the threshold for 1099-K forms would be lowered to $600, rather than $20,000/200 sales. However, the IRS announced on Nov. 21, 2023 that this tax season would be treated as another transition year, keeping the old threshold limits in place.

Additionally, as a continuation of the phase-in for the new thresholds, the tax year for 2024 will move to a $5000 threshold.

"Following feedback from taxpayers, tax professionals and payment processors and to reduce taxpayer confusion, the Internal Revenue Service today released Notice 2023-74 announcing a delay of the new $600 Form 1099-K reporting threshold for third party settlement organizations for calendar year 2023.

As the IRS continues to work to implement the new law, the agency will treat 2023 as an additional transition year. This will reduce the potential confusion caused by the distribution of an estimated 44 million Forms 1099-K sent to many taxpayers who wouldn't expect one and may not have a tax obligation. As a result, reporting will not be required unless the taxpayer receives over $20,000 and has more than 200 transactions in 2023.

Given the complexity of the new provision, the large number of individual taxpayers affected and the need for stakeholders to have certainty with enough lead time, the IRS is planning for a threshold of $5,000 for tax year 2024 as part of a phase-in to implement the $600 reporting threshold enacted under the American Rescue Plan (ARP)."

Keep in mind that if you’re going to receive Form 1099-K, you should receive it by January 31. Third-party payment processors are allowed by law to send the form to you electronically or by mail.

What should you do with Form 1099-K?

If you do receive Form 1099-K, the first thing you should do is compare it to your own financial records. It isn’t unheard of for payment processors to make a mistake. If they accidentally report to the IRS that you made more money than you actually did, you could get stuck on the hook paying taxes on money you didn’t actually earn!

Before you worry if this number doesn’t match, keep in mind a couple of things. Form 1099-K only takes into account your gross sales. For that reason, it doesn’t consider or report:

- Fees (i.e. PayPal fees, marketplace fees, etc.)

- Refunds and returns

- Shipping and postage

- Business expenses like packaging supplies, etc.

If you determine that your 1099-K is incorrect, contact the third-party payment processor that issued it immediately. If you’ve determined that your 1099-K matches your own records, then put it up for safekeeping. This is an informational return, so there’s no need to do anything else with it. Your payment processor has already sent it on to the IRS.

Related: IRS FAQs on payment card and third-party network transactions

Form 1099-K for GoDaddy Payments customers

To improve the tax reporting experience for our customers using GoDaddy Payments, we have automated the Form 1099-K process. With this rollout, GoDaddy Payments customers will be able to access and download a PDF/electronic copy of their Form 1099-K from the new Tax Center in the Payments Hub.

What will the IRS do with Form 1099-K?

Form 1099-K is supposed to ensure that we’re all paying our fair share of income tax. So if a third-party payment processor reports that you made $75,000 in income, while you tell the IRS you only made $74,000 in income, you need to have the financial records and documentation ready to back up any discrepancies. Otherwise, your tax return could be red-flagged for further scrutiny.

Tax season can feel stressful for small business owners, so hopefully this guide has helped to shed some light on Form 1099-K and the steps you may need to take ahead of filing. And, if you’re interested in more automation in the future for your Form 1099-K, GoDaddy Payments has you covered.