When you start an LLC, it’s an exciting time for a business owner, but it can also be daunting. There’s a lot to think about, from paperwork and certification to registration and more.

In this six-step guide, we’re making the process as simple as possible. We’ll take you through the LLC journey from picking a name to registration and forming your LLC. It’s important to note that how you start an LLC will depend on the state you’re in, so check local legislation as you go. There are also several types of LLCs available, each with their own advantages and disadvantages, for more on this you can check out our list of different types of LLCs.

Disclaimer: This content should not be construed as legal or financial advice. Always consult an attorney or financial advisor regarding your specific legal or financial situation.

What is an LLC?

So, what is an LLC? An LLC, or Limited Liability Company, is a business structure that creates a boundary between your personal assets and your business. Think of it as a protective shield that separates what you own personally from your business’s finances.

When you start LLC formation, you’re setting up a legal divide between your personal belongings and your business.

LLCs are popular for their mix of structure and flexibility. You can choose to run an LLC on your own as a “single-member LLC” or with others as a “multi-member LLC.” There’s also no need for formal board or officer titles, which gives you more control over the organization and management of the business.

What type of LLC should you set up?

Thinking about taking that next big step toward becoming an LLC? The first choice you'll face is deciding on the type that suits your business best. There are several types of LLCs available, each with its own advantages and disadvantages. For more on this, you can check out our list of different types of LLCs.

If you’re curious about how to open up an LLC that matches your goals, here’s a quick breakdown of the main types:

- Single-member LLC: Ideal for solo entrepreneurs, this LLC type lets you be the sole decision-maker. You get personal liability protection and a straightforward setup without the need to coordinate with anyone else. Think of it as the “go-it-alone” option with big benefits. A single-member LLC has some similarities with a sole proprietorship, you can see a full comparison between the two in Sole proprietorship vs LLC: Which is right for your business?

- Multi-member LLC: If you have business partners, this type is the way to go. A multi-member LLC allows you to share the workload, profits, and responsibilities. With an Operating Agreement, you and your partners can clearly define roles and set up fair profit-sharing.

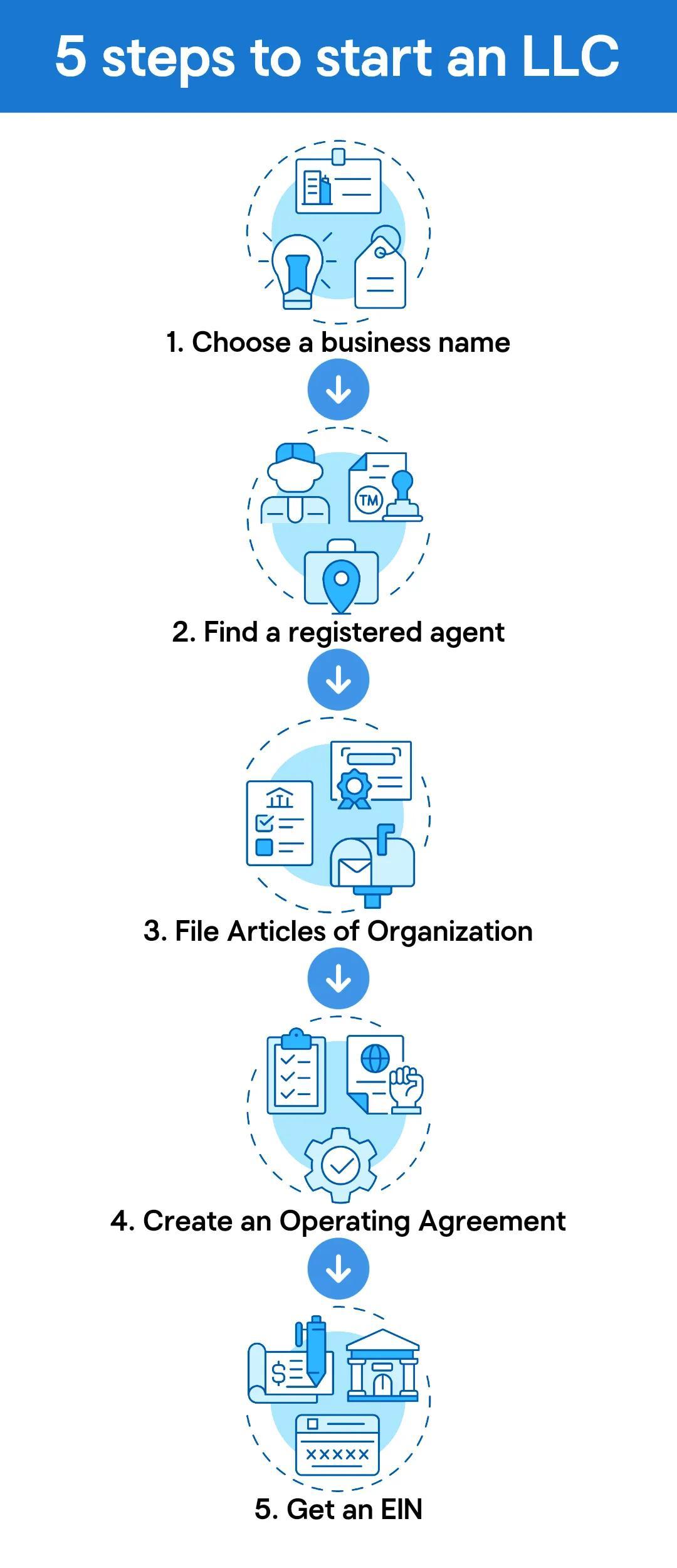

5 steps to start an LLC

1. Choose a name for your LLC

Every business needs a name, but it’s easy as an entrepreneur to overlook this point. Before registering your business to become an LLC, make sure the name is available. The last thing you want is to choose a name for your LLC to find it's already in use or trademarked. You can learn how to check if your business name is taken in this guide.

There may be state restrictions on words you can use within your business name. Restricted words might include ‘bank,’ ‘trust,’ ‘trustee,’ or ‘corporation.’ Basically, your business name must reflect your business and not be misleading. However, LLC formation requirements, including choosing a name, vary by state.

For state-specific information, check the articles below.

Related: How to register a business

Register your business domain name

After finding the perfect name, register a domain name that matches it. This will help protect your branding and make it easier for customers to find you online. Once you’ve registered your domain, you can create your website for your own online business. For more information on the importance of domains, check out the video below.

Get a DBA

Not sure what is a DBA? A DBA, or “Doing Business As,” is a registered name that allows your business to operate under a brand name different from its legal name. For example, if your company is registered as Smith Holdings LLC but you want to market your services as Bright Start Marketing, you would file a DBA to legally use that name. Many LLCs choose a DBA to create a more memorable brand, launch a new product line, or target a different audience without forming a new legal entity.

2. Find a registered agent in your state

Appointing a registered agent is a must-do in the process of starting an LLC. Your registered agent will generally need to have a physical address in the state in which your LLC is registering.

The role of the LLC registered agent is to pass important documentation to key personnel within the LLC. Your registered agent will forward documentation such as legal notices and tax forms. Your registered agent should notify you of any legal issues at your earliest convenience. It’s an important role, and if someone within the company is going to take it, they need to be diligent.

In many cases, the option for a registered agent service is highly desirable. This way, you can hire someone (or a company) to handle the legal and administrative tasks of being a registered agent. Hiring someone is especially useful if there’s no one qualified or happy to take on that role within the LLC. Or, if there’s no physical address within the state the company is registering in.

You can learn more about registered agents, including how to be one yourself or how to hire one, in our what is a registered agent guide.

3. File the Articles of Organization (Certificate of Formation)

Your Articles of Organization (aka. Certification of Formation) is a form that you can pick up from your local government agency, like the Secretary of State.

You will need to file the form and provide the information required. Each state has its own form, so it’s important to make sure you’ve picked up the correct one. You can expect to fill out your typical information, such as the company name, business address, and names and addresses of the LLC owners.

You’ll also need to designate an LLC organizer, who is responsible for filing the formation documents with the state.

4. Create an Operating Agreement for your LLC

Your Operating Agreement is a bit like a contract between owners. The document is legally binding and outlines how the LLC will be managed. Even if it’s not required by law, having one is incredibly helpful, especially as your business grows. In this guide, you can learn more about what is an Operating agreement and how to create one.

Importantly, the Operating Agreement is in place to outline how profits and losses are shared and could be used to resolve potential future conflicts. When creating this agreement, it can be helpful to work with a lawyer.

Here’s a look at the key questions your Operating Agreement should answer:

- Who owns what? Clearly list each member and what percentage of the LLC they own. This keeps ownership clear and straightforward.

- Who does what? Outline roles and responsibilities for each member. This could include managing finances, handling daily operations, or leading certain projects.

- How are decisions made? Decide on the process for making big decisions. Will everyone get an equal vote, or will certain choices require a majority?

- How are profits and losses split? Describe how you’ll divide profits (and any losses). Will it be based on ownership shares or something else?

- What happens if someone leaves or joins? Set guidelines for what to do if a member wants to leave or a new person wants to join. This keeps things simple and prevents future issues.

- How will we dissolve the LLC if needed? Outline the steps for closing the LLC if you ever need to. This helps everyone know what to expect if it comes to that.

The agreement means that all owners are aligned on some of the most important aspects of starting an LLC.

5. Get an EIN (Employer Identification Number)

Your EIN (Employer Identification Number) is a federal identification number issued by the IRS and acts as your LLC’s unique identifier for taxes. It is essential for many types of activities, including opening a business bank account, hiring employees, filing taxes, applying for licenses and permits, and more.

Essentially, your EIN proves you’re an established business.

Even if you’re not planning to hire employees immediately, having an EIN makes it easier to manage your business finances separately from personal ones and gives your LLC a professional edge. You can apply online directly through the IRS website. Setting up your EIN brings you one step closer to a fully functioning, legitimate business.

Not sure which business tax IDs your LLC needs? Read our “What’s the difference between EIN and TIN” article.

How long does it take to get an EIN?

You typically receive your EIN immediately when you apply online. If you choose to apply by fax or mail, it can take up to 4 weeks.

How much does an EIN cost?

No matter which state your LLC is based in, it is completely free to get and maintain an EIN.

How much does it cost to start and run an LLC?

When submitting your formation paperwork, you’ll need to pay a state filing fee. The cost to start an LLC depends entirely on where you’re forming it. Some states keep it budget-friendly. For example, Colorado charges just $50 to file Articles of Organization, making it one of the more affordable options. On the higher end, Massachusetts requires a $500 filing fee, which is among the most expensive in the country.

But the filing fee is only part of the picture. Many states also require an annual report fee to keep your LLC in good standing. In Massachusetts, the annual report costs $500 each year. In Colorado, the periodic report fee is $25. That means your first-year total could be around $75 in Colorado, compared to about $1,000 in Massachusetts when you factor in both formation and the first annual report.

You may also need to budget for optional costs like a registered agent service, business licenses, or a DBA if you plan to operate under a different name. Since fees and requirements vary widely, always check your specific state’s LLC guide to understand the exact costs you’ll be responsible for before you file.

What to do after starting an LLC

You filed your paperwork, and your LLC is official. Now it’s time to set up the systems that keep your business compliant and financially organized.

Open a business bank account

Keeping your business finances separate protects your personal assets, makes accounting much easier, and builds credibility with customers and vendors. To open an LLC bank account, you’ll typically need:

- Your approved Articles of Organization

- Your EIN

- Your operating agreement

- A valid government-issued ID

File annual reports

Most states require LLCs to file an annual or periodic report to stay in good standing. This filing updates your business information, such as your address and registered agent, and usually includes a fee. A few states, including Arizona and New Mexico, don’t require a traditional annual report. Others use a different system. Alabama, for instance, requires a Business Privilege Tax instead.

Deadlines and fees vary, so check your state’s specific requirements. Staying on top of your LLC annual report helps you avoid penalties, late fees, or administrative dissolution.

Get local business permits and licenses

Some businesses need federal, state, county, or city permits and licenses to operate legally. Requirements depend on your industry and location. To determine what your LLC needs, check your state’s business portal, then visit your city or county clerk’s website for local rules.

Understand your taxes

By default, LLCs are pass-through entities, meaning profits and losses flow through to your personal tax return. Depending on your state and situation, you may elect corporate tax treatment instead.

You may be responsible for federal income tax, state income tax, self-employment tax, and possibly sales tax. You can use a sales tax calculator to estimate what you owe, and review guidance on filing business taxes for LLC to make sure you’re on the right track.

LLC vs. sole proprietorship vs. corporation

Undecided on whether an LLC is the right business structure? If that’s the case, you’re likely comparing a sole proprietorship vs LLC and a corporation (Inc.) vs LLC. Let’s take a look at each one:

- Sole proprietorship: The simplest structure with no legal separation between you and your business. It’s easy and low-cost to start, but you’re personally responsible for all debts and legal obligations.

- LLC (Limited Liability Company): A flexible structure that creates a separate legal entity. It helps protect your personal assets and typically offers pass-through taxation, with the option to choose corporate tax treatment.

- Corporation: A formal legal entity separate from its owners. It provides strong liability protection and can raise capital through stock, but it requires more paperwork, compliance, and ongoing administrative responsibilities.

Use the table below to better understand how these business structures differ.

| Feature | Sole Proprietorship | LLC | Corporation (S-Corp & C-Corp) |

|---|---|---|---|

| Formation complexity | Easiest | Moderate | Most complex |

| Cost to start | $0-50 | $50-500 | $100-800+ |

| Liability protection | ❌ None | ✅ Yes | ✅ Yes |

| Taxation | Pass-through (personal) | Pass-through (flexible) | S-Corp: Pass-through C-Corp: Double taxation |

| Paperwork/compliance | Minimal | Moderate | Extensive |

| Ownership structure | One owner only | One or more members | Shareholders |

| Best for | Freelancers, solo contractors | Small to medium businesses | Growing businesses, investors |

Starting an LLC in your state

For most entrepreneurs, the best place to form an LLC is your home state — where you live and actively do business. In fact, about 90% of small business owners are better off registering locally. It’s usually simpler, more affordable, and helps you avoid the extra paperwork and double registration fees that can come with forming in another state.

If you form your LLC out of state, keep in mind that you’ll likely still need to register in your home state as a foreign LLC. That means paying fees in both states and maintaining compliance in both places.

Planning for the future? Learn how to transfer an LLC to another state.

Your questions about starting an LLC, answered

It’s common to have a lot of questions before deciding whether or not to make the leap into an LLC business. Here, we’re answering commonly asked questions.

Additionally, learning how to write a business plan can help you formalize a strategy that'll keep your ideas on track. You can also check our free business plan template.

What is the lifespan of an LLC?

The lifespan of an LLC varies by state. Some require it to be 30 years or indefinite, and it can continue until the owners dissolve it.

How do you make money with an LLC?

An LLC makes money the same way any business does: by selling products or services at a profit. Your revenue depends on your business model, pricing strategy, and ability to attract and retain customers. LLC owners, known as members, can earn money in a few ways, depending on how their LLC is taxed:

- Owner draws: Taking money out of the business profits.

- Salary: If the LLC is taxed as an S corporation, owners can pay themselves a reasonable salary.

- Profit distributions: Dividing profits among members based on ownership percentages.

Should I pay myself a salary from my LLC?

You should seek financial support before deciding how to pay yourself through your LLC, but, as above, there’s an option to pay for contracted hours of service that benefit the business. Or, as the owner, you can take distributions.

Can I use my personal money for my LLC?

As a business owner, you can use personal money to fund an LLC. This is particularly common in the early days of starting an LLC.

Can I transfer money from my LLC to my personal account?

Transferring money from your LLC to a personal account is also legal, but it’s important to document it correctly. If you are actively working on day-to-day operations, you should be classified as an employee and pay yourself a reasonable salary, just like any other employee.

As an LLC owner, you may also take distributions of the LLC’s profits. These are not subject to payroll taxes. Just remember to record each distribution to avoid any tax complications.

Do LLC owners get W-2?

Typically, the answer is no. If you’re setting up a limited liability company and only receiving distributions of the LLC’s profits, you will need to file a 1099-NEC. If you decide to pay yourself a salary as an employee, then you would get a W-2 just like any other employee on payroll.

Choosing between a W-2 and a 1099-NEC affects your taxes. With a W-2, taxes are automatically withheld, so you’re set for tax season. But if you’re getting a 1099-NEC, no taxes are taken out upfront. You’ll need to set aside money for self-employment taxes (e.g. Social Security and Medicare) on your own. Without careful planning, this can lead to a surprise tax bill or even penalties. Read this guide to business taxes to learn more.

How much does an LLC usually cost?

The cost to form an LLC depends on your state. Filing fees typically range from about $50 to $500, with most states landing somewhere in the middle. You may also need to budget for annual report fees, registered agent services, business licenses, or a DBA if you plan to operate under a different name. Always check your state’s official requirements to get an accurate cost estimate.

Can I make an LLC by myself?

Yes, you can form an LLC on your own. Most states allow you to file formation documents directly through the Secretary of State’s website. You’ll need to choose a business name, appoint a registered agent, file Articles of Organization, and create an operating agreement. While many business owners handle this themselves, others choose to use a formation service to save time and reduce the risk of errors.

How long does it take to start an LLC?

The timeline varies by state and filing method. Online filings can be approved in a few business days in some states, while others may take a few weeks. Expedited processing may be available for an additional fee.

What are the benefits of an LLC?

The biggest benefit of an LLC is that it offers liability protection, meaning your personal assets are generally protected from business debts and lawsuits. It also provides flexible tax options, including pass-through taxation by default. LLCs require less ongoing paperwork than corporations while still offering credibility and structure. For many small business owners, it strikes a balance between simplicity and protection.

Final thoughts on starting an LLC

Starting an LLC is a big step toward building something of your own. While the process varies slightly by state, the core steps are straightforward: choose your name, file your formation documents, stay compliant, and set up your business for long-term success. When you understand the requirements and plan ahead for ongoing responsibilities, forming an LLC becomes much more manageable.

If you’re ready to make it official, you don’t have to do it alone. You can get free LLC setup with GoDaddy and take the next step toward launching your business today.